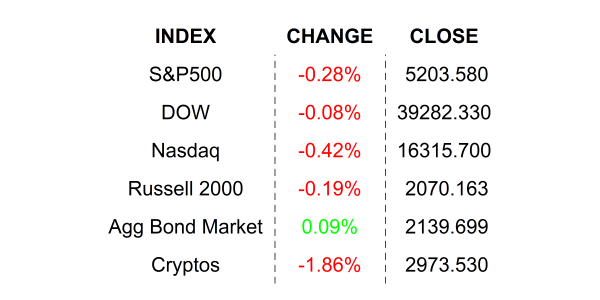

Stocks fell yesterday, giving up earlier gains late in the session as traders became bored with a lack of any news. Consumer confidence is waning according to the latest report from the Conference Board – it could spell future trouble for GDP.

How can they afford that? Come on, you know you have done it. You are driving with your partner or your friends, and you pass a beautiful home or a swanky sportscar, and someone shakes their head and says, “I don’t know how people can afford those things.” Another blurts out “DEBT, they probably have a bunch of debt.” Well, I can’t tell you for certain if that statement is true, but I can tell you that, indeed lots of people use debt to purchase homes and cars, and I can tell you that it is perfectly normal and not unhealthy… UNLESS you can’t afford to make the payments AND you realize that the value of the asset you purchased using that debt is technically lower than its market value. In other words, if you want to sell it, you have to first pay back your lender before you can get any gains or invested principal back. No problem, if it is sold at a gain. In fact, the return on your original investment is higher with leverage if you sell at a gain. HOWEVER, if you sell at a loss, your loss is greater with leverage. You are probably well aware of this by now. But let’s take this concept into the world of commercial real estate.

This morning as I prepared to write this report WHILE YOU SLEPT, I came across a simple one-line blurb. It read something like “Defaulted Downtown LA office tower sold for 50% of outstanding debt.” Now, most people would just keep scrolling and not think much of that, but I stared at it for a moment and remembered that I wrote about it last year when its then owner Brookfield Asset Management first suggested that it may default on it and essentially, “turn in the keys.” Why would they do that? Well, most commercial real estate is leveraged, and that leverage can go as high as 80% with all sorts of complicated clauses. The 80% thing is not a problem, as long as the owner can afford to pay debt service, as in, MAKE THE PAYMENTS. The owner uses receipts from leases in the property. If your rent roll is $5000 and your debt service is $4000, congratulations, you have positive cash flow. If that building goes up in value and you sell it 10 years later, congratulations, you made positive cash flow for 10 years, completely depreciated the asset offsetting taxes, and you made a hefty, levered return on your investment.

You, my regular reader, are astute, and you realize that it can’t be that simple. Actually, it is THAT simple, however in order for our fictional investor to get that win a few assumptions had to be made. First, the property had to go up in value and second, rent roll had to stay constant or increase, and third, debt service had to remain constant or go down. If rent roll goes down or debt services goes up, our fictional real estate investor only has $1000 wiggle room before having negative cash flow, which is the equivalent to burning money in your sleep… um, not so good. How can that happen? Let’s start with the obvious. Rent roll can decrease for 2 primary reasons, vacancy or lower rents. Did you know that LA is the second largest US city? Go ahead, check me on that. According to a recent report from real estate giant JLL, the vacancy rate for LA’s central business district was some 22.7%. This can be translated into the owner of that building, the 777 Tower, making -22.7% less rent roll than its potential. That is bad but may not be the real problem. In fact, smart real estate analysts at Brookfield probably factored in the possibility of 80% occupancy when they underwrote the building. However, rent means income, and income IN ALL CASES is good, but let’s get to the kicker. Most real estate debt is either short-term or floating and is collateralized with the underlying asset. In our fictional example, the investor possibly had a 4 or 5 year CRE loan and had to refinance half way through the investment cycle. Assuming that the investor kept the same amount of debt, refinancing could cause debt service to change, affecting monthly cash flow. If prevailing interest rates go down, the investor could make more money, but if they go up… uh, oh.

Back to downtown LA. Interest rates, as you probably know by now, not only went up, but they went up by a lot in 2022 and they stayed high. If any real estate investor had a loan maturing since March of 2022, they would be paying higher monthly debt service because of the increase in interest rates. Vacancy rates nearly doubled in LA from the start of 2022 and SOFR (Secured Overnight Financing Rate), the rate at which most CRE loans are based on, went from 0.5% to 5.31%. All that means that if an LA real estate investor had to refinance in that period, their cash flow would be lower, and likely, negative. If that real estate investor borrowed on a floating rate, regardless of refinancing, his or her monthly debt service would have adjusted in steps and increased with the SOFR rate… also bad. Ahh, but the story gets even more twisted. Remember that we talked about leverage that is based on the value of the real estate that collateralized the loan. As rates went higher and vacancies grew, real estate values declined. According to Green Street, office CRE fell by -14% in the past year. If a lender was only willing to loan up to 80% on collateral, the amount that a borrower could acquire would be lower, so refinancing may have required the investment of additional principal. It gets worse yet. Lenders, knowing that the market was soft have tightened their collateral requirements to cover the potential risk of default, which made it even harder to refinance. That, my friends is how South Korean investment firm Consensus just picked up the posh 777 Tower for 50% of its outstanding debt.

Let’s take a tally of the players involved. Brookfield is in the business of taking risk, so this default is simply egg on its face. The folks who lent Brookfield the money, which included banks and investment companies were the losers in the affair. Consensus Asset Management, the new buyers are the winners… assuming that the value of the property doesn’t go down further, vacancy rates don’t go higher, and interest rates don’t go up, because Consensus bought the property using… you guessed it… DEBT.

WHAT’S UP IN THE PREMARKET

Merck & Co Inc (MRK) shares are higher by +4.60 in the premarket after the company announced that it got FDA approval for its hypertension drug Winrevair. The announcement is good timing for Merck as Keytruda approaches the end of its exclusivity lifecycle. Good timing also for those original real estate investors in the 777 Tower 😉. Merck will announce its Q1 earnings later next month. Dividend yield: 2.45%. Potential average analyst target upside: +8.7%.

YESTERDAY’S MARKETS

NEXT UP

- MBA Mortgage Applications (March 22) declined by -0.7% for the week after declining by -1.6% in the prior week.

- Fed Governor Christopher Waller will speak today.

IMPORTANT DISCLOSURES.

Muriel Siebert & Co., LLC is an affiliated broker/dealer of the public holding company, Siebert Financial Corporation, which also owns Siebert AdvisorNXT, LLC. Siebert AdvisorNXT, LLC is a registered investments advisor (RIA) with the SEC and with state securities regulators. We may only transact business or render personal investment advice in states where we are registered, filed notice or otherwise excluded or exempted from registration requirements. Investment Advisor products are NOT insured by the FDIC, SIPC any federal government agency or Siebert’s parent company or affiliates.

You are being provided this Market Note for general informational purposes only. It is not intended to predict or guarantee the future performance of any security, market sector or the markets generally. This Market Note does not describe our investment services, recommendations or market timing nor does it constitute an offer to sell or any solicitation to buy. All investors are advised to conduct their own independent research before making a purchase decision. This Market Note is to provide general investment education and you are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate for you based on certain investment objectives and financial situation. Do not use the information contained in this email as a basis for investment decisions. You should always consult your investment advisor and tax professional regarding your investment situation before investing. The charts and graphs are obtained from sources believed to be reliable however Siebert AdvisorNXT does not warrant or guarantee the accuracy of the information. Any retransmission, dissemination or other use of this email is prohibited. If you are not the intended recipient, delete the email from your system and contact the sender. This is a market commentary, not research under FINRA Rule 2210 (b)(1)(D)(iii) and FINRA Rule 2210 (c)(7)(C).

© 2021 Siebert AdvisorNXT All rights reserved.