Stocks traded lower Friday, but for some mega cap tech stocks which were unwilling to give up ground. Traders took a break after a busy week of whipping and driving, accentuated the directionless equities in Friday’s session.

And now… what. The Fed told us what it was thinking. If you missed it, FOMC members put their own forecasts out there, including where they thought Fed Funds policy would put the key interest rate by yearend. Economically speaking, the Fed raised its forecast for GDP up to +2.1% from +1.4%, Unemployment Rate down to 4.0% from 4.1%. and Core Inflation UP to +2.6% from +2.4%. All great except maybe inflation, right? That is a problem if a) you, like the rest of us, are trying to stick to a budget, and b) you, LIKE THE REST OF US, own lots of interest rate sensitive growth stocks. Fed cuts have been rally cry number 2 in the recent bullish binge in tech stocks… of course, behind rally cry number 1, AI. Given this information, one would surely conclude that the Fed would come out with some sort of bearish policy change, or at least some sort of hawkish signaling. But that didn’t really happen. The central bankers stuck to their December interest rate target which implies 3 rate cuts of -25 basis points through the end of the year. At first glance that would be an everything-coming-up-roses projection for stocks.

Getting technical, we see that FOMC members raised their Fed Funds Projections slightly in 2025, 2026, and so-called “Longer run”. Logically, that is most likely a response to the Fed’s improved GDP projections this year through 2026. The slightly tighter interest rate policy was noted and largely excused by markets which rallied last Wednesday and Thursday. On the path of rate cuts, the market is finally in sync with the Fed. Overnight Index Swaps now predict a 100% chance of 3 cuts and a 22% chance of a fourth. For some frame of reference, swaps were predicting twice that amount just 2 months ago. And with that, blue chip economists are indicating a 40% chance of recession in the next 12 months, down from 50% in January. Oh, and the 2-year / 10-year yield curve is still inverted, which is a well-known, historically, high-probability market predictor of recession. In fact, the curve flattened further, that is, it got more inverted since January, which may imply higher probability of recession according to the market.

Are you confused yet? Don’t be. Just pay attention to what Jerome Powell told us outside the numbers and the official statement. He talked about how it would be appropriate to slow down quantitative tightening. He implied strongly that the Fed would be willing to tolerate short-term inflation target overshoots. He also implied that the Fed wanted to avoid job-cut momentum. WOW, in case you didn’t know, that is the first real mention of the Fed’s OTHER mandate since its hawkish pivot in late 2021. When the Fed is worried about unemployment, it usually comes with looser monetary policy. This, combined with the projections I mentioned a few paragraphs and 1 lukewarm espresso ago, implies that, according to the most power economists in the world, the US economy is healthy and that they will not stand in its way, FOR NOW. So, for now, let’s just say all is good.

In the week ahead, we will get the Fed’s favorite inflation figure PCE Deflator which surely, the FOMC had an early glimpse of. So, any shockers are likely to be lower. If they are higher, the Fed is clearly not concerned. I will be watching Consumer Confidence closely, because that is the ember that sparks consumption which is good for the economy, and it has been languishing in the past year. I will also be paying close attention to the first wave of FOMC members to get out and speak after last week’s policy meeting. They like to talk, as I am sure you know, and they will likely parrot their positions from last week’s forecast. It should be noted that most folks talk about the median projections, which are statistically meaningless without knowing at least the range of those projections. For example, at least 2 FOMC members expect Fed Funds to remain unchanged by yearend. We can expect those members to attempt to throw cold water on the bulls. Ok, I have droned on too long about this. The bottom line is that the Fed is OK for the moment. In the weeks ahead we must take a hard look at companies themselves and determine if they can live up to the great things their stock prices currently suggest.

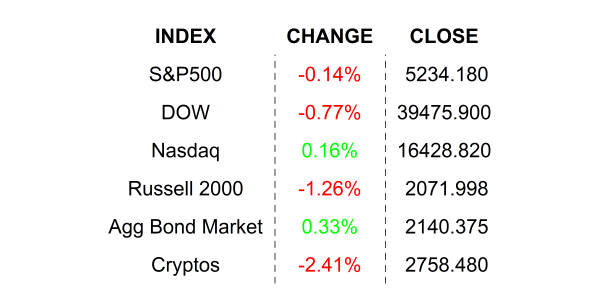

FRIDAY’S MARKETS

NEXT UP

- Chicago Fed National Activity Index (Feb) is expected to come in at -0.34, slightly lower than the prior months -0.30 print.

- New Home sales (Feb) may have increased by +2.1% after climbing by +1.5 in January.

- Fed speakers: Bostic, Goolsbee, and Cook.

- The week ahead: more housing numbers, Conference Board Consumer Confidence, more regional Fed reports, GDP Revisions, Personal Income, Personal Spending, PCE Deflator, and University of Michigan Sentiment. Check the attached weekly economic calendar for times and details. Also check out my daily chartbook which will give you further insight into important indexes. Lastly, remember that you can check out all of my posts from the last 5 years here: https://www.siebert.com/blog/

IMPORTANT DISCLOSURES.

Muriel Siebert & Co., LLC is an affiliated broker/dealer of the public holding company, Siebert Financial Corporation, which also owns Siebert AdvisorNXT, LLC. Siebert AdvisorNXT, LLC is a registered investments advisor (RIA) with the SEC and with state securities regulators. We may only transact business or render personal investment advice in states where we are registered, filed notice or otherwise excluded or exempted from registration requirements. Investment Advisor products are NOT insured by the FDIC, SIPC any federal government agency or Siebert’s parent company or affiliates.

You are being provided this Market Note for general informational purposes only. It is not intended to predict or guarantee the future performance of any security, market sector or the markets generally. This Market Note does not describe our investment services, recommendations or market timing nor does it constitute an offer to sell or any solicitation to buy. All investors are advised to conduct their own independent research before making a purchase decision. This Market Note is to provide general investment education and you are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate for you based on certain investment objectives and financial situation. Do not use the information contained in this email as a basis for investment decisions. You should always consult your investment advisor and tax professional regarding your investment situation before investing. The charts and graphs are obtained from sources believed to be reliable however Siebert AdvisorNXT does not warrant or guarantee the accuracy of the information. Any retransmission, dissemination or other use of this email is prohibited. If you are not the intended recipient, delete the email from your system and contact the sender. This is a market commentary, not research under FINRA Rule 2210 (b)(1)(D)(iii) and FINRA Rule 2210 (c)(7)(C).

© 2021 Siebert AdvisorNXT All rights reserved.